Self-managed super funds are about to lose the ability to borrow for residential property, and the change arrived faster than almost anyone expected. Here is a calm, clear read on the SMSF residential borrowing ban: what happened, what we know, what we still do not, and how to make sense of the timing.

This article is general information and commentary only. It is not financial, legal or taxation advice, it does not consider your objectives, financial situation or needs, and it is subject to change without notice. ASPIRE Accredited Advisors provide property investment advice only. If self-managed super funds are relevant to you, please seek your own licensed professional advice before acting.

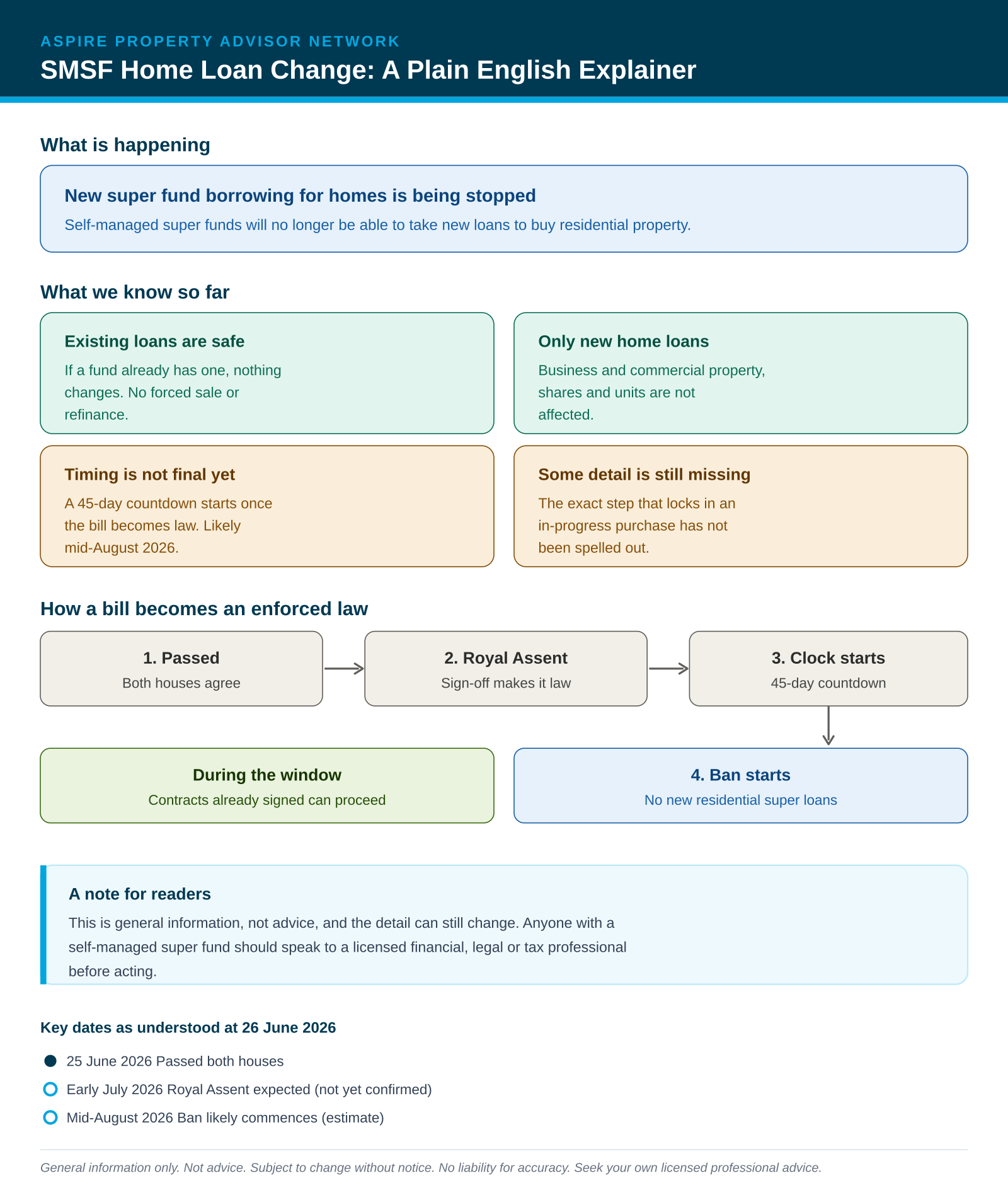

There are weeks where Canberra moves slowly, and then there are weeks like this one. On Thursday 25 June the government's tax reform bill passed both houses of Parliament, and tucked inside it was a late change that caught a lot of people off guard. Self-managed super funds are going to be stopped from borrowing to buy residential property.

This is a commentary on what we know so far, not advice. The headlines have been loud and the detail has been thin, so it is worth walking through properly. The most important thing to watch is the gap between when something passes Parliament and when it actually bites, because that gap is where most of the current confusion is sitting.

What happened with the SMSF residential borrowing ban

A self-managed super fund, or SMSF, is a super fund you run yourself. For years, one of the things a fund could do was borrow money to buy an investment property, using a structure called a limited recourse borrowing arrangement, which people in the industry shorten to LRBA. That borrowing route, for residential property, is being closed.

The change was not in the government's original Budget. It came in as the price of Greens support in the Senate for the broader tax reform bill, and the amendment removes residential property from the assets an SMSF can acquire under a borrowing arrangement. Business real property stays in, so the SMSF residential borrowing ban is aimed squarely at homes bought with new loans inside super.

What we actually know

A few things are now reasonably clear, and they are worth holding onto before the commentary runs away with itself.

If a fund already holds a residential property bought with one of these loans, nothing changes. No forced sale, no required refinance, no unwinding. The change only looks forward.

Borrowing to buy commercial or business real property is untouched, as are shares and units in a trust. A fund can still own residential property outright. It is borrowing to buy a home inside super that is being stopped.

The other thing we know is that the timing does not run off the day Parliament passed the bill. It runs off a later step called Royal Assent, which is worth understanding properly, because it is the part most people skip over.

What we do not know yet

Some of the detail genuinely is not settled, and it would be dishonest to pretend otherwise.

When a purchase is locked in

If someone is partway through a purchase, the exact step that protects their deal, whether it is finance approval, signing the loan, the contract of sale, the deposit or the bare trust deed, has not been spelled out. Until the ATO or Treasury clarifies it, anyone mid-transaction should be getting specific legal advice rather than guessing.

The mid-August estimate depends on a Royal Assent date that has not yet happened, and on instruments that have not yet been released. It is an estimate, not a fixed date, and a second technical bill is expected later in the year to fill in carve-outs.

How a change like this becomes enforceable

This is the bit worth slowing down on, because it explains why you are seeing dates like mid-August floating around when the bill only passed last week.

Passing Parliament is not the same as becoming law. A bill can clear both houses and still not be in force. It becomes an actual Act only when it receives Royal Assent, the formal sign-off given by the Governor-General. That is usually a formality once a bill has passed, but it is a separate step with its own date.

For this change, that Assent date is the starting gun. The ban does not switch on the day Parliament passed it. Instead, a 45-day countdown begins once Assent is given, and the ban takes effect at the end of it. Parliament passed the bill on 25 June, and the winter break is due to start on 2 July, so Assent is widely expected in early July. Work forward 45 days and you land around mid-August. That is where the estimate comes from, and it will shift if Assent comes earlier or later.

During that 45-day window, deals that are already signed can keep going. The window exists precisely so that arrangements already underway can reach completion. It is a transition, not an invitation to start a new purchase late and rely on the clock.

Where this fits with the bigger tax changes

The borrowing ban hitched a ride on a much larger bill, and two of the other changes in it are worth knowing about, even though they do not start until 1 July 2027.

The first is the capital gains tax discount. From mid-2027 the long-standing 50 per cent discount for individuals and trusts is being replaced with an inflation-based system and a minimum tax rate on gains made after that date. Gains built up before then still get the old discount, so anything held across the changeover gets split.

The second is negative gearing. From the 2027 to 28 year, negative gearing on residential investment properties bought after Budget night this year is being tightened. Importantly, super funds are carved out of that particular change, and properties already held at Budget night are exempt. A second, more technical bill is expected later in the year to tidy up the carve-outs, so this is not the final word.

How to read this

When a change moves this fast, the noise tends to run ahead of the facts. The facts here are actually fairly contained. Existing arrangements are protected, the change is about new residential borrowing inside super, and the timing depends on a sign-off date that has not happened yet.

What it does not change is the value of getting the right people around you. If you have a self-managed super fund, or you were thinking about using one to buy property, this is exactly the moment to talk to a licensed financial adviser, along with your accountant and a solicitor who knows this area. The detail is still settling, the lender market may move before the law does, and the cost of getting the timing wrong is real. ASPIRE will keep watching the detail as it firms up.

Nothing in this is advice. It is general information only and is subject to change without notice. The timing depends on a Royal Assent date not yet confirmed, key concepts in the package remain undefined, and the lender market may move ahead of the law. Please seek your own licensed financial, legal and taxation advice before making any decision.

References

Listed in order of authority: official government and parliamentary sources first, then professional and industry commentary, then media coverage. Links current at the time of writing and subject to change.

Official government and parliamentary sources

Treasury Ministers, second reading speech, Treasury Laws Amendment (Tax Reform No. 1) Bill 2026

Professional and industry commentary

SMSF Adviser, LRBAs will soon be limited to business real property and exclude residential property

PwC Australia, 2026-27 Federal Budget, CGT and housing tax reform

Corrs Chambers Westgarth, capital gains tax and negative gearing amendments

Media coverage

The Adviser, government agrees to ban future LRBA for residential property

Broker Daily, MFAA calls for certainty as tax reforms pass Senate and House

Australian Financial Review, SMSF property plans and the Labor-Greens budget deal

Disclaimer. This article has been prepared by ASPIRE Property Advisor Network as general information and commentary for the public. It does not constitute financial, legal or taxation advice and does not consider any individual's objectives, financial situation or needs. ASPIRE Accredited Advisors provide property investment advice only and do not provide superannuation, taxation, accounting, legal or financial product advice. Legislative timing and detail described here remain subject to Royal Assent and to further legislative instruments and may change without notice. No liability is accepted for the accuracy of information relied on to create this article. Readers must obtain their own licensed professional advice before making any decision. Self-managed super funds are a complex area and require advice from licensed professionals.